Co-Sell in Financial Services: What Works

What is co-sell in financial services?

Short answer: Co-sell in financial services is the joint selling motion run into banks, insurers, and asset managers, where vendor risk reviews, procurement gates, and regulatory constraints shape every step. It works the same way co-sell works anywhere, but it has to clear a buyer environment that other sectors never see.

The motion itself does not change. Two companies still account-map overlap, run a deal-review cadence, ship enablement, and track attribution. What changes is the buyer. A financial-services customer wraps any purchase in third-party risk management, security review, and procurement process that can add months to a cycle.

That buyer environment is why co-sell in financial services deserves its own playbook. A co-sell motion tuned for fast-moving software buyers will stall the first time it hits a bank’s vendor onboarding queue. The partnerships team that wins in this sector designs the motion around the gates instead of being surprised by them.

This post covers what stays the same, what changes, and the specific adjustments that keep a financial-services co-sell deal moving through the compliance and procurement steps that would otherwise kill it.

Why co-sell in financial services matters in 2026

Three forces have made this a sector worth a dedicated approach. Financial-services buyers increasingly prefer to buy through trusted, already-approved vendors and partners, which makes co-sell a structural advantage rather than a nicety. Third-party risk scrutiny has tightened across the sector, so a partner that is already an approved vendor at a bank can carry a co-seller through a gate that would take a newcomer two quarters. And the deal sizes in this sector are large enough that a longer cycle is still worth running well.

The case for a tuned motion has three layers. At the strategy layer, a partner with an existing footprint at a financial institution is an access asset; co-sell turns that footprint into a shared pipeline. At the operating layer, the compliance and procurement gates are predictable, so they can be planned into the deal review instead of discovered late. At the financial layer, the cost of a co-sell deal stalling in vendor onboarding for two quarters is real, and most of it is avoidable with earlier sequencing.

The reality most teams live is a co-sell motion that runs fine until it hits the first procurement gate, then goes dark. The partnerships team treats the stall as bad luck. It was not luck. The gate was always there, and the motion was never designed to clear it.

How co-sell in financial services actually works

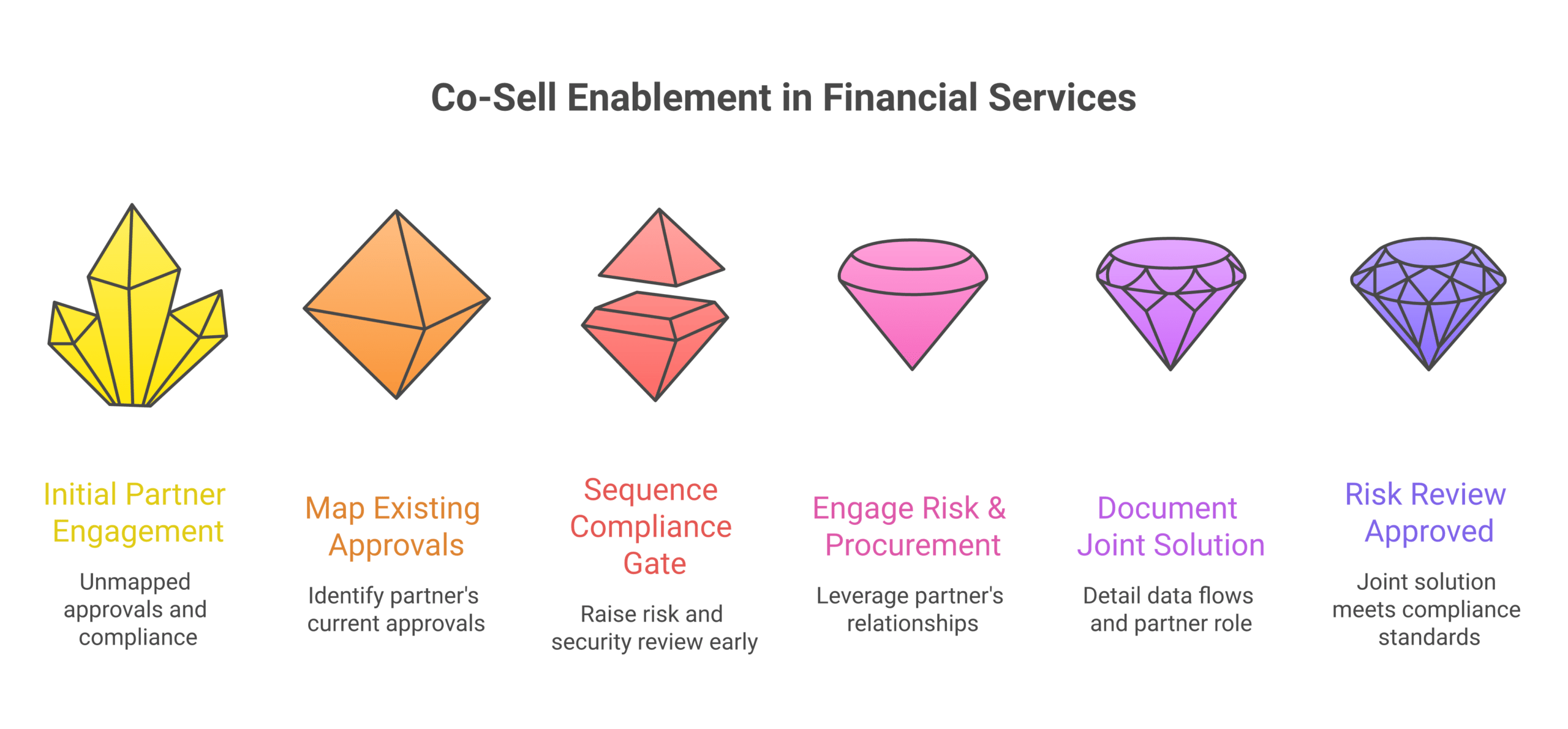

The motion adds four sector-specific adjustments on top of the standard co-sell mechanics. Each one addresses a gate the financial-services buyer puts in the path.

- Map the partner’s existing approvals first: Before account mapping for overlap, find out where the partner is already an approved vendor. A partner already through risk review at a target institution is the single biggest accelerator in the sector. That approval status is part of the overlap picture.

- Sequence the compliance gate early: The customer’s third-party risk and security review should be raised in the first joint customer conversation, not discovered at procurement. The deal review tracks the compliance milestone as a deal stage, with a named owner on the vendor side.

- Bring the partner’s risk and procurement relationships into the motion: The partner often knows the institution’s procurement lead and risk team. Co-sell enablement in this sector includes mapping those relationships, not just the buying-committee sellers.

- Document the joint solution for the risk review, not just the pitch: Financial-services risk teams evaluate the combined solution, including data flows and where the partner sits in the architecture. The joint pursuit playbook needs a risk-facing description, not only a customer-facing one.

The closing point is that these four adjustments share one principle: pull the gates forward. The standard co-sell motion treats compliance and procurement as things that happen at the end. The financial-services motion treats them as deal stages with owners and dates, raised early, tracked in the deal review. The gate does not move; the surprise does.

Common pitfalls

Co-sell failures in financial services are consistent, and almost all of them come from running a sector-blind motion.

- Discovering the compliance gate late: The deal moves well until procurement, then the third-party risk review surfaces and adds two quarters nobody planned for.

- Ignoring the partner’s approval status: The team account-maps for sales overlap but never checks where the partner is already an approved vendor, missing the fastest path in.

- A customer-only joint solution doc: The pursuit playbook describes the pitch but not the data flows and architecture a risk team needs. The risk review then stalls on missing information.

- Treating procurement as administrative: The team assumes procurement is a rubber stamp after the business decision. In this sector procurement is a real evaluation with its own timeline.

- Co-selling with a partner with no footprint: Pairing with a partner that is also a newcomer at the institution. Two unapproved vendors do not clear a gate faster than one.

What this looks like in practice

Co-sell in financial services runs on the standard stack plus closer attention to the compliance record. The tools do not change; what gets tracked in them does.

A software vendor wants into a regional bank. Direct, it faces a full third-party risk review and a vendor onboarding queue measured in quarters. Instead it co-sells with a partner that is already an approved vendor at the bank. The partnerships team maps the partner’s approval status first, raises the compliance question in the first joint customer call, documents the combined solution with a risk-facing architecture description, and tracks the compliance milestone as a deal stage in the weekly review. The risk review still happens, but it runs in parallel with the sales process instead of after it. The deal closes in two quarters rather than four.

The contrast is the same vendor running a sector-blind co-sell motion. Strong pitch, good partner, but the compliance gate surfaces at procurement and nobody owned it. The deal adds two quarters and the partnership gets blamed.

Forecastable’s POV

The mistake vendors make in financial-services co-sell is treating the sector like every other, just slower. It is not just slower. It has gates that other sectors do not have, and those gates either get planned into the motion or they ambush it. A co-sell program that wins in financial services is not more patient. It is better sequenced.

Across our client base, the single highest-leverage move in this sector is choosing the partner for its approval footprint, not only its sales relationships. A partner already through risk review at a target institution can carry a co-seller through a gate that would take a newcomer two quarters to clear alone. That footprint is worth more than a warm intro, and most partnerships teams never check for it because their account mapping only looks at sales overlap.

The contrarian point is that the compliance gate is an asset, not an obstacle, when you co-sell correctly. The same gate that slows you down is the moat that keeps the next vendor out once you and your partner are through it. The teams that resent the gate run worse motions than the teams that design around it.

If you are co-selling into financial services, pick partners for their approvals, pull the compliance gate forward into the first customer call, and track it as a deal stage with an owner.

Forecastable is an independent third-party professional services company. Our evaluations of co-sell motions and tooling are based on publicly-available information as of May 2026 and our own client experience.

Frequently asked questions

How is co-sell in financial services different from other sectors?

The motion is the same, but the buyer adds third-party risk review, security evaluation, and a real procurement process that can extend cycles by quarters.

What makes a good co-sell partner in financial services?

A partner already an approved vendor at the target institutions. That existing approval footprint is the biggest single accelerator in the sector.

When should the compliance gate be raised?

In the first joint customer conversation. Raised early, the risk review runs in parallel with the sales process. Discovered late, it adds quarters.

Does co-sell shorten financial-services sales cycles?

It can, when the partner has an existing approval footprint and the compliance milestones are sequenced early. It does not shorten cycles if the motion is run sector-blind.

What does the joint pursuit playbook need for this sector?

A risk-facing description of the combined solution, including data flows and architecture, alongside the customer-facing pitch. Risk teams evaluate the joint solution, not just the sales story.

Should you co-sell into a bank with a partner that has no footprint there?

Rarely. Two unapproved vendors do not clear a risk gate faster than one. Pick a partner with standing at the institution.

Next step

If your co-sell deals in financial services keep stalling at procurement, the gate is not the problem. The motion was never designed for it. Pick partners for their approval footprint, raise compliance in the first customer call, and track it as a deal stage.

Talk to our team about co-sell in regulated sectors →

The co-sell hub holds the broader operating context, and the co-sell motion write-up covers the base mechanics this sector builds on.