AWS Marketplace Co-Sell: The Motion Most ISVs Skip

What is AWS Marketplace co-sell?

Short answer: AWS Marketplace co-sell is the sales motion where an ISV transacts a deal through AWS Marketplace while simultaneously working the opportunity with an AWS field seller through the ACE (AWS Customer Engagements) system. It pairs a private offer with a registered, accepted opportunity, so the AWS rep gets quota credit and the customer gets EDP burndown.

It is not a listing strategy. It is not a billing migration. It is a co-selling motion that happens to use Marketplace as the transaction venue, and the difference matters because the mechanics that produce the win sit outside the listing itself.

A working version of this motion has three properties. First, every Marketplace transaction tied to a competitive sales cycle has a corresponding ACE opportunity that the AWS rep has accepted. Second, the private offer is constructed with the AWS field rep in the loop on terms, timing, and customer context. Third, the joint pursuit is run as one sales cycle with two sellers, not as two parallel processes that converge at the signature page.

Adjacent terms worth pinning down: a Marketplace transaction is the act of a customer purchasing your software through their AWS bill. A Marketplace listing is the product page and metering setup. AWS Marketplace co-sell is the field motion that produces the transaction. Confusing them is the most common reason ISVs report Marketplace revenue but no AWS field traction.

Why AWS Marketplace co-sell matters in 2026

Three forces sharpened the question this year. AWS Enterprise Discount Programs are renewing at scale, and customers want every eligible spend to count against their committed spend. The AWS field comp plan continues to reward Marketplace-transacted, ACE-accepted opportunities at a higher rate than direct ISV deals. And procurement teams at mid-market and enterprise accounts are asking the buying question early in the cycle, not as a closing detail.

The three-layer operating case is straightforward. Layer one is the buyer, who wants EDP burndown, consolidated billing, and a procurement path that does not require a new vendor onboarding. Layer two is the AWS field seller, who needs co-sold ACV to hit a plan that has shifted hard toward partner-influenced revenue. Layer three is the ISV, which gets cycle acceleration, larger deals, and APN tier credit when the motion is run cleanly.

This is operating reality, not a thought experiment. ISVs that run the full motion close the AWS-influenced portion of their pipeline materially faster, at larger deal sizes, with higher net retention because the AWS rep is on the renewal as well. ISVs that treat Marketplace as passive plumbing get the billing benefit and almost none of the sales benefit, which is the worst trade in the catalog. For broader industry context, see AWS Partner Co-Sell Program documentation.

How AWS Marketplace co-sell actually works

The motion is mechanical. It runs the same way whether you are selling a data platform, a security tool, or an observability product, with the same five components moving in the same order.

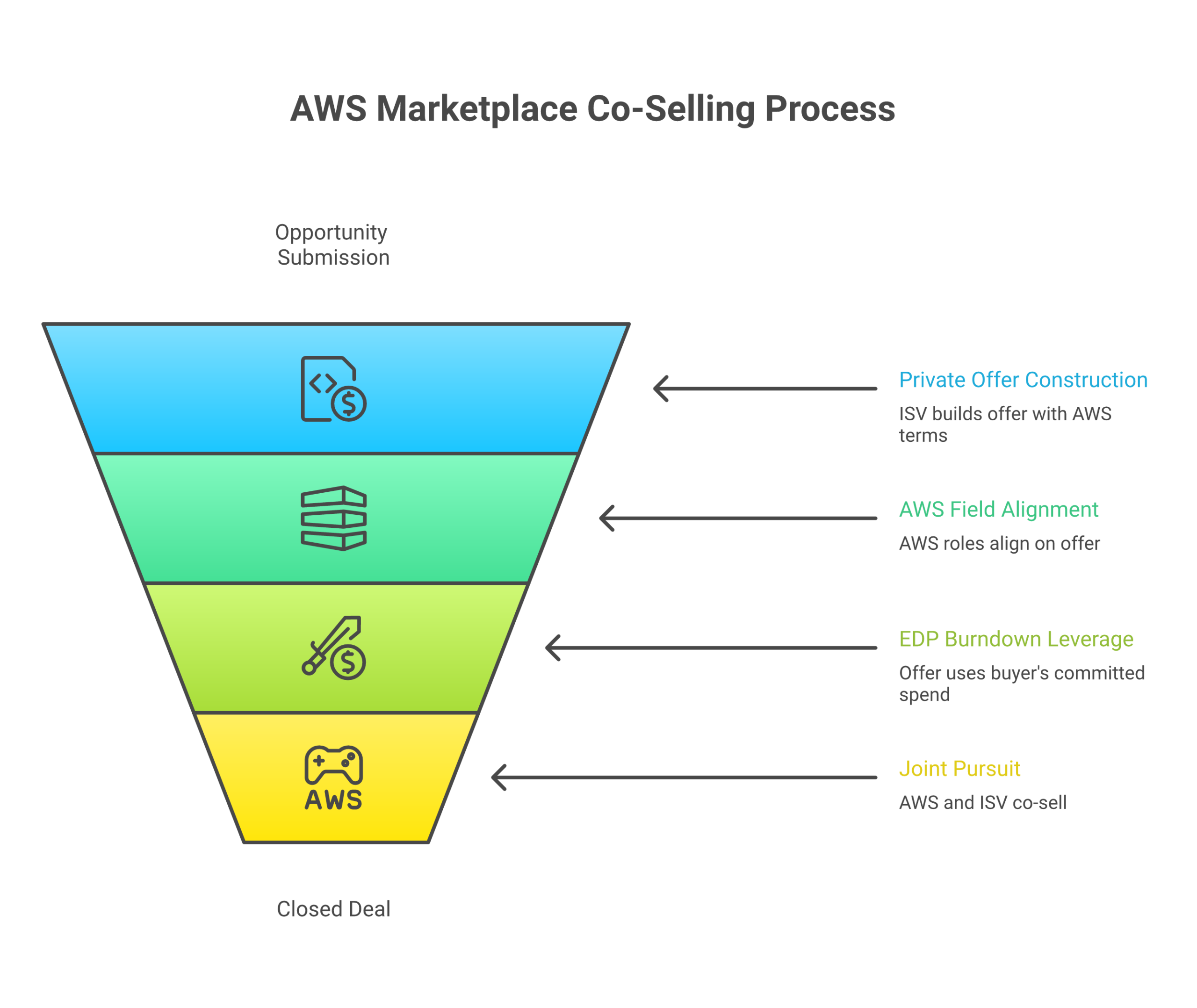

- ACE opportunity submission and acceptance: The ISV submits the opportunity into ACE early, ideally at qualified pipeline stage, with enough detail that the AWS rep can accept it inside the SLA. Acceptance is the trigger that puts the deal on the AWS field plan and unlocks co-sell support, not a back-office formality.

- Private offer construction with AWS-eligible terms: The ISV builds a private offer in Marketplace with pricing, payment schedule, and contract length that the customer’s procurement team can sign. The terms should reflect the deal the AWS rep and ISV rep negotiated, not a standalone price list. EDP-eligible pricing is the default, not the exception.

- AWS field rep alignment (PDM and ISM): The Partner Development Manager and the Industry Sales Manager are the two AWS field roles that determine whether your opportunity gets pulled into account planning. Aligning early means joint account reviews, warm introductions inside the customer org, and a co-owned close plan that survives procurement.

- EDP burndown leverage as the buyer’s mechanical reason: Most enterprise customers have committed spend they are trying to consume. A Marketplace transaction with a private offer counts against that commitment. Naming this in the discovery conversation, in the proposal, and in the order form is the difference between “interesting” and “we have to buy it this way.”

- Joint pursuit motion with the co-selling AWS rep: The two sellers run the cycle together. Joint discovery calls, shared next steps, mutual close plan, mutual escalation when procurement stalls. The ACE opportunity gets updated with stage changes so the AWS rep’s forecast reflects reality, which is how trust gets built for the next deal.

The cadence is the operating reality. ISVs that win on this motion review ACE opportunity status weekly with their AWS PDM, refresh stage and amount before AWS forecast calls, and treat the AWS field rep as a co-seller with shared responsibility for the close date. That cadence is what produces the acceleration; the listing and the private offer are necessary, not sufficient.

Common pitfalls

These show up in almost every diagnosis we run on an underperforming AWS Marketplace co-sell motion.

- Submitting ACE opportunities late or never: The ISV closes the deal direct, then drops the transaction into Marketplace at signature. The AWS rep gets the credit after the fact, learns nothing about the cycle, and has no reason to bring you into the next account. The motion fails to compound.

- Treating private offers as a discount mechanism instead of a sales motion: Sales teams use private offers because the customer asked for a custom price, not because the ISV is running an AWS co-sell play. The PDM is not in the loop, the ISM does not know the deal exists, and the buyer gets confused about who the actual seller is.

- No internal owner for the AWS motion: The Marketplace listing sits with finance or product, the AWS field relationship sits with partnerships, and the deal sits with sales. Nobody owns the connective tissue. The motion falls between three orgs every time the deal needs a decision.

- Ignoring EDP burndown in qualifying conversations: Discovery skips the procurement question, so the team finds out at week ten that the customer has $4M in EDP commitment they need to consume. By then the deal is structured as a direct contract and rebuilding it through Marketplace adds a month to the cycle.

- Confusing Marketplace revenue with co-sell traction: The board deck shows growing Marketplace ARR and the team concludes the partnership is working. Most of that revenue is existing customers shifting their billing, not net new logos won with AWS field help. The co-sell motion never actually started.

Tools and examples

The tooling stack splits cleanly into three layers, and most teams underinvest in the middle one.

| Layer | What it does for AWS Marketplace co-sell | Examples |

|---|---|---|

| Marketplace listing and private offer tooling | Manages product listing, metering, private offer construction, contract terms, renewal mechanics | Tackle, Labra, Suger, Clazar, AWS-native Marketplace Management Portal |

| Co-sell motion and overlap tooling | Identifies overlap with AWS field accounts, surfaces co-sell opportunities, tracks joint pipeline, integrates with ACE | ACE itself, Crossbeam |

| Revenue ops and attribution | Syncs Marketplace and ACE data into Salesforce, attributes partner influence, reports on AWS-sourced and AWS-influenced pipeline | Salesforce with APN and ACE sync, CRM partner attribution layers, RevOps data pipelines |

A worked example to make the numbers concrete. Take a mid-stage data ISV with a $40K average ACV and a 90-day enterprise sales cycle. When the team runs the full motion (ACE submitted at qualified, PDM in the weekly forecast call, private offer aligned with AWS rep, EDP burndown named in discovery), ACE-accepted opportunities close 30 to 45 percent faster, with 8 to 12 percent larger ACV, and a 20 to 30 point lift in win rate versus the non-ACE control. The biggest single contributor is not the discount, it is the AWS rep co-selling inside the account.

Forecastable’s POV

Most ISVs we talk to think they are running AWS Marketplace co-sell because they have a listing, a private offer template, and somewhere between three and twelve closed Marketplace deals. They are running a Marketplace transaction motion, which is a different thing, and the gap is costing them the part of their pipeline they actually wanted from the partnership.

The contrarian position is simple. AWS Marketplace is not your closing mechanism. ACE is. The ISV teams that treat ACE acceptance as the leading indicator (and the PDM cadence as the operating rhythm) get a measurably different business out of the AWS partnership than the teams that treat Marketplace as a checkout page. The first cohort builds compounding AWS field relationships and wins net-new logos with co-sellers. The second cohort migrates existing revenue to a different billing rail and calls it a win.

We have seen this play out across a range of client motions. The teams that invest in the connective tissue (an internal owner for the AWS motion, a weekly ACE hygiene cadence, discovery scripts that surface EDP commitment in the first call) get the acceleration. The teams that bolt private offers onto a direct sales cycle get the Marketplace listing fee and not much else. The mechanical difference is small. The revenue difference is not.

The other position worth defending publicly: the right tools stack matters less than the operating rhythm. We are agnostic on whether you use Tackle, Labra, Suger, or Clazar for the Marketplace side, and on whether you use Crossbeam, Pocus, or Common Room for overlap. We care a great deal that the motion has a named owner, a weekly ACE review, a real PDM relationship, and a measurement system that separates AWS-sourced, AWS-influenced, and AWS-transacted revenue. That is the operating reality of working AWS Marketplace co-sell.

Forecastable is an independent third-party professional services company. Our evaluations of AWS Marketplace co-sell motions are based on publicly-available information as of May 2026 and our own client experience.

Frequently asked questions

Is AWS Marketplace co-sell the same as listing on Marketplace?

No. Listing is the product setup. Co-sell is the field motion. You can have an active listing and zero co-sell traction, and you can run co-sell motions that converge to a Marketplace transaction only at the close. Treating the two as the same is the most common diagnostic finding when we audit an underperforming AWS partnership.

Do I need to submit every deal into ACE?

For competitive, partner-influenced deals where you want the AWS rep co-selling, yes. For pure renewals of existing customers with no AWS field involvement, no. The rule of thumb is that an opportunity belongs in ACE if you want the AWS field on the deal, and an AWS field rep cannot help you on a deal they cannot see.

What is the difference between APN, ACE, and Marketplace?

APN is the partner program (tiers, certifications, benefits). ACE is the opportunity management system inside APN that handles joint pipeline and co-sell tracking. Marketplace is the transaction and billing venue. The three connect: APN tier unlocks ACE access, ACE-accepted opportunities can convert to Marketplace transactions, and Marketplace transactions feed back into APN tier criteria.

How does EDP burndown actually work for the buyer?

A customer’s Enterprise Discount Program commitment is dollars they have promised AWS they will spend. A Marketplace transaction with an eligible private offer counts against that commitment. So a $300K software purchase through Marketplace consumes $300K of the customer’s EDP commitment, which is usually the cleanest path for the customer to consume committed spend on something other than infrastructure.

Who owns the AWS Marketplace co-sell motion internally?

There is no single right answer, but there has to be a single owner. The most common working model is a partnerships leader who owns the AWS relationship, a partner sales manager or co-sell lead who owns the motion week to week, and a RevOps partner who owns the data plumbing. What does not work is leaving the motion distributed across product, finance, and sales with no named accountability.

Does the AWS rep care about my deal if it is under six figures?

Less than they care about a seven-figure deal, but more than you think. AWS field reps have account-level partner-influence quotas, and smaller deals in priority accounts often matter more than larger deals in non-priority accounts. The honest answer is that you find out by building the PDM relationship and asking which accounts in your territory are priorities this quarter.

Should I use Tackle, Labra, Suger, or Clazar for the listing side?

The honest answer is that all four are capable, and the right choice depends on your existing tech stack, your contract complexity, and where you want the operational ownership to sit. We have seen working motions on each. We have not seen the choice of Marketplace tooling be the determining factor in whether the co-sell motion works.

Next step

If you are reading this and thinking your team has the listing but not the motion, you are in the most common position we see. The fix is not more tooling. The fix is a named owner, a weekly ACE cadence with your PDM, discovery scripts that surface EDP commitment in the first call, and a measurement system that separates Marketplace transactions from AWS-influenced revenue. That is a four-week project, not a four-quarter rebuild.

Talk to our team about your AWS Marketplace co-sell motion →

The co-sell hub holds the broader context on how AWS Marketplace co-sell fits inside a broader hyperscaler and ISV co-sell strategy.